From petrol prices to mortgage rates, the US-Israel war with Iran has already had an impact on people's finances in the UK.

How deep and sustained that turns out to be depends on the duration of the conflict and how quickly supply lines and economies can recover.

Here are some of the areas to watch out for.

Fuel prices for motorists

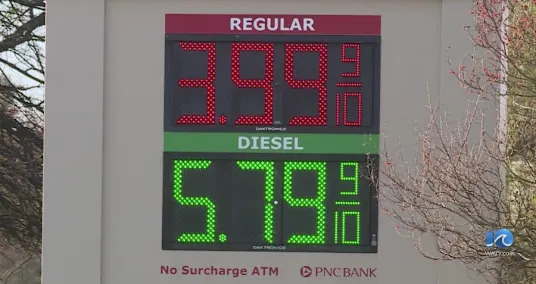

Drivers may have already noticed that prices at the pump are on the rise.

By Friday, average petrol prices hit 150.11p a litre, up by 17.3p since the start of the conflict, while diesel had increased by 35.3p to 177.68p, the RAC motoring organisation said.

Earlier this month, the increase in pump prices triggered a row between petrol retailers and the government. Retailers accused the government of using "inflammatory language" by suggesting firms were profiteering from the oil price surge.

According to analysts, every $10 increase in oil pushes up pump prices by roughly 7p a litre.

Crude prices have risen sharply since the start of the war, although they are volatile as they react to the status of the conflict and commentary from the White House.

While motoring organisations say that there are plenty of supplies, they are encouraging people to reduce non-essential journeys. They also suggest people amend their driving style, by not accelerating or braking too hard to conserve fuel.

Not everyone has a car or may not use one for a daily commute. However, when petrol rises, it can carry through to higher prices for goods and services.

For example, if transport costs for supermarkets increase that could then be reflected in the cost of food.

Cost and choice of mortgages

Before the war began, there had been a hope and expectation of a steady fall in the interest rates charged on new, fixed mortgages, as well as lower variable rates.

Now, the opposite is happening.

Lenders have raised rates quickly, owing to their own funding costs rising and an expectation that the base borrowing rate will not fall as previously anticipated.

The average two-year fixed rate has jumped from 4.83% at the start of March to 5.75% now, its highest since last March, according to the financial information service Moneyfacts. The cheapest deals have risen the fastest.

For those looking for a five-year deal, the average rate has gone up from 4.95% to 5.69% over the same period and is now at its highest level since July 2024.

At times of economic uncertainty, lenders pull mortgage products off the shelves, reducing choice.

There are now 1,620 fewer residential mortgage products on the market, according to Moneyfacts, although that still leaves more than 6,000 deals to choose from.

NEUESTE BEITRÄGE

- 1

Insane Realities That Will Make You Reconsider How you might interpret History30.06.2023

Insane Realities That Will Make You Reconsider How you might interpret History30.06.2023 - 2What will happen if Artemis 2 astronauts get hit by a solar storm during NASA's ambitious moon mission?31.03.2026

- 3Ariana Grande says Eternal Sunshine 2026 tour will be her last for a 'long, long time': 'One last hurrah'18.11.2025

- 4Pain at the pump for Hampton Roads residents03.04.2026

- 5'Something Very Bad Is Going to Happen' is the Duffer Brothers' first project since 'Stranger Things.' It's also 'wildly insane.'25.03.2026

Ähnliche Artikel

- Glamour Shots once ruled the mall. I went to one of the last ones standing.02.01.2026

- Death toll from floods in Afghanistan rises to 6104.04.2026

- At UN climate conference, some activists and scientists want more talk on reforming agriculture21.11.2025

- The Longest Underwater Tunnel Connecting Germany and Denmark14.01.2026

- Ten Awesome Authentic Realities That Will Leave You Interested30.06.2023

- What happened to Eleven after the ambiguous 'Stranger Things' series finale? Millie Bobby Brown knows — but 'swore herself to secrecy'05.01.2026

- Well known Worldwide Caf\u00e9s to Experience05.06.2024

- Cuba says 33 have died of mosquito-borne illnesses as epidemic rages01.12.2025

- Israel says 40 Hezbollah members killed as forces advance in Lebanon02.04.2026

- ByHeart sued over recalled formula by parents of infants sickened with botulism15.11.2025